We speak with people every day about Health Savings Accounts (HSAs) and most of them just don’t understand how they work. Let’s face it, the government regulates these things so it can be confusing. That's why we're here, to help it all make sense.

HSA Basics

HSA’s have been around since 2003 and have quickly become one of the best ways to help control the rising cost of health coverage. So, here is our effort at trying to explain them!

There are 2 parts to an HSA: Part 1, you have a Qualified High Deductible Health Plan (QHDHP) through an insurance company. This is your health insurance. Part 2, a special bank account called a Health Savings Account (HSA) that allows you to pay for healthcare expenses tax free. Because you have part 1 you can legally have part 2. To help confuse you, people use the term HSA to refer to both the QHDHP and the actual HSA bank account.

Part 1

What is a QHDHP?

Well it changes a little every year but, for 2024:

• Minimum $1600 single or $3200 family deductible

• No first dollar coverage or copays – except for preventive care

• Must be filed with the state as a QHDHP

Part 2 – The cool part

What is an HSA?

This is an actual bank account. It can be at any bank that offers HSA’s (most banks now). This account is usually free of charge (If it’s not, you may want to try a different bank) and earns interest.

The money you put in this account is tax free and can be used for any “qualifying medical expense.” This means that the expense has to fall within certain IRS guidelines, which is probably more than you would expect! For example:

• All the normal stuff – Doctor & Hospital expenses, prescriptions

• Vision exams, contacts, glasses

• Dental expenses (non-cosmetic)

• Over the Counter drugs – If you have a prescription from your doctor.

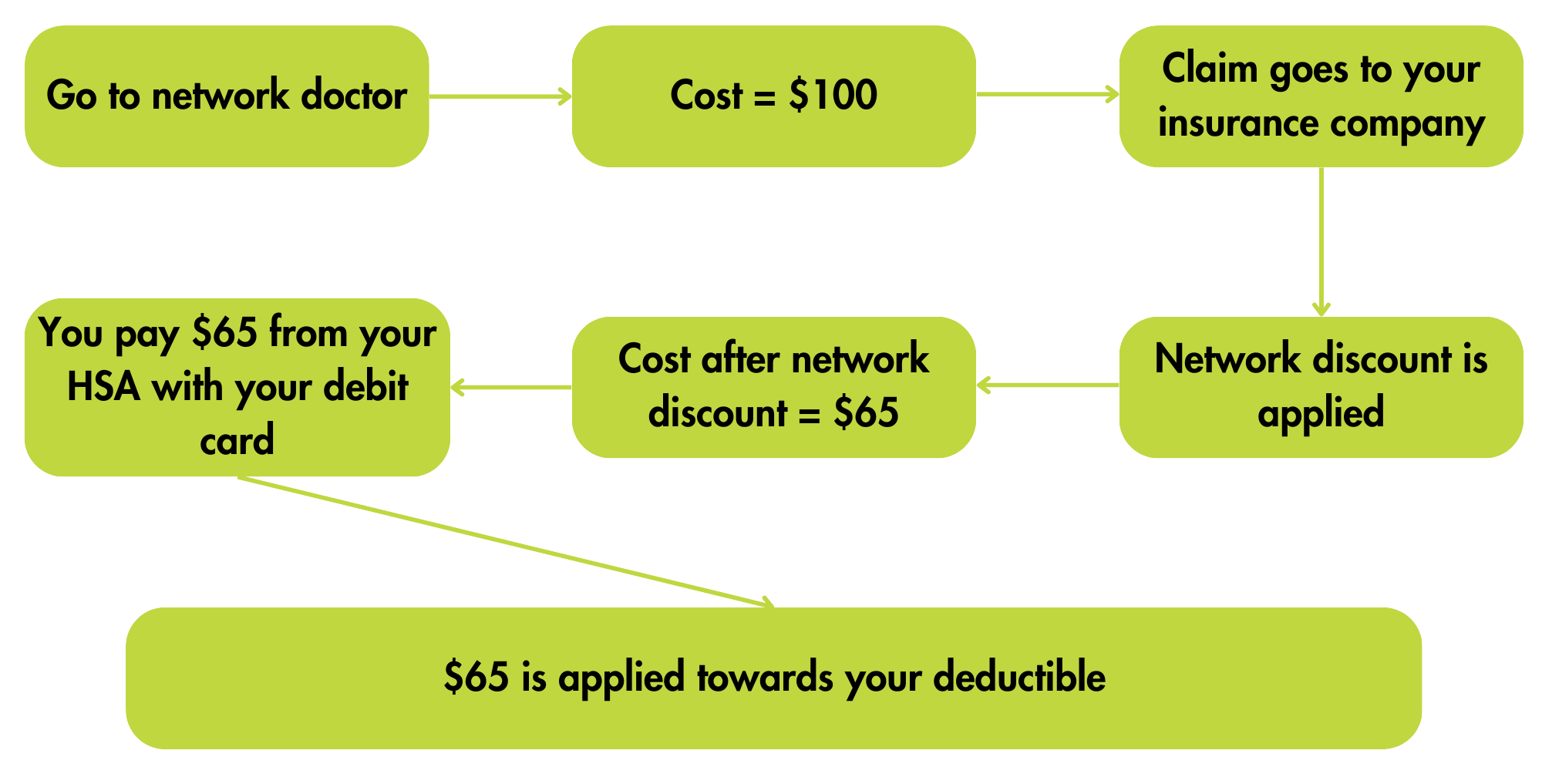

Ok, so now let's see how this would work if you had some medical expenses. Let's say you have an insurance plan that has a $2000 deductible and 100% coinsurance. (Plan pays 100% after you meet the deductible.)

Claim #1

Claim #2

HSA Qualified Expenses

The following contains a list of qualified and non-qualified medical expenses. This list is intended to provide a quick guide.

For more details refer to IRS Publication 502 or speak with a tax advisor.

Abortion

Acupuncture

Alcoholism treatment

Ambulance services

Anesthetists

Artificial limbs

Bandages

Birth control pills (by prescription)

Breast reconstruction surgery (mastectomy)

Blood tests

Braces

Orthopedist

Braille books/magazines

Car modifications required for accessibility

Chiropractor

Christian Science Practitioner

Contact lenses

Crutches

Dental treatment (except cosmetic treatment)

Dentures

Dermatologist

Diagnostic devices and fees (includes expenses related to diagnosing & treating illness such as blood sugar tests for diabetics)

Disabled dependent care

Drug addiction therapy (covers inpatient treatment including meals & lodging)

Eyeglasses

Eye surgery (includes laser eye treatments)

Fertility treatments

Guide dogs

Hearing aids

InsulinLaboratory tests

Insurance premiums (only if receiving unemployment benefits)

Lead based paint removal (only removal, not repainting)

Medicare Part B Premiums

Medicare Part D Premiums

Nursing services

Obstetrician

Ophthalmologist

Operations (except cosmetic)

Optician

Oral Surgery

Orthopedic Shoes

Out-of-pocket expenses for your spouse/dependent Oxygen (for equipment to relieve breathing problems)

Physician

Postnatal treatments

Prenatal care

Prescription drugs

Prosthesis

Psychiatric care

Psychoanalysis

Registered nurse

Splints

Sterilization

Stop

Smoking Programs (except non prescription drugs) Transportation and essential to medical care

Vaccines

Vasectomy

Vision correction surgery

Weight loss programs (only amounts related to treatment for specific diseases)

Wheelchairs X-rays;

Contribution Limits

2025

Individual Maximum Contribution: $4,300

Family Maximum Contribution: $8,550

HSA Catch-up Contributions (age 55 or older*): $1,000

2024

Individual Maximum Contribution: $4150

Family Maximum Contribution: $8300

HSA Catch-up Contributions (age 55 or older*): $1,000

* Catch-up contributions can be made any time during the year in which the HSA participant turns 55.